Market Commentary - 03/19

What a wild few months it’s been. Long gone are the calm, smooth waters of 2017. 2018 ended with a bang – or a crash! The dip in October as more rate hikes were foreshadowed was followed by a midterm election induced rally in November. Then the bottom fell out during the worst December since the Great Depression.

The reasons for the December fallout are very apparent – the Fed signaled more tightening amid a slowing global economy which spooked investors (and moreso the trading algorithms). But three months later the market has sprinted back to 2800+ and volatility has been cut in half. This has occurred despite 2019 S&P earnings estimates getting trimmed from $178 to a range closer to $170-172 (approx. 5% year over year growth). Therefore, the market’s valuation on 2019 earnings has expanded from <14x at the end of December to 16.4x. A 50-point band around 2800 on the S&P feels reasonable for now given a confluence of factors following the 500-point run-up since the December 24th bottom: slowing global growth, US dollar strength, and 10-year US interest rates falling quickly (see below). There does seem to be some belief that 2020 S&P earnings can again grow by 5-6% to the low $180/share range, making a 2900 target within reach later this year if global growth trends are not worsening and further rate hikes remain shelved.

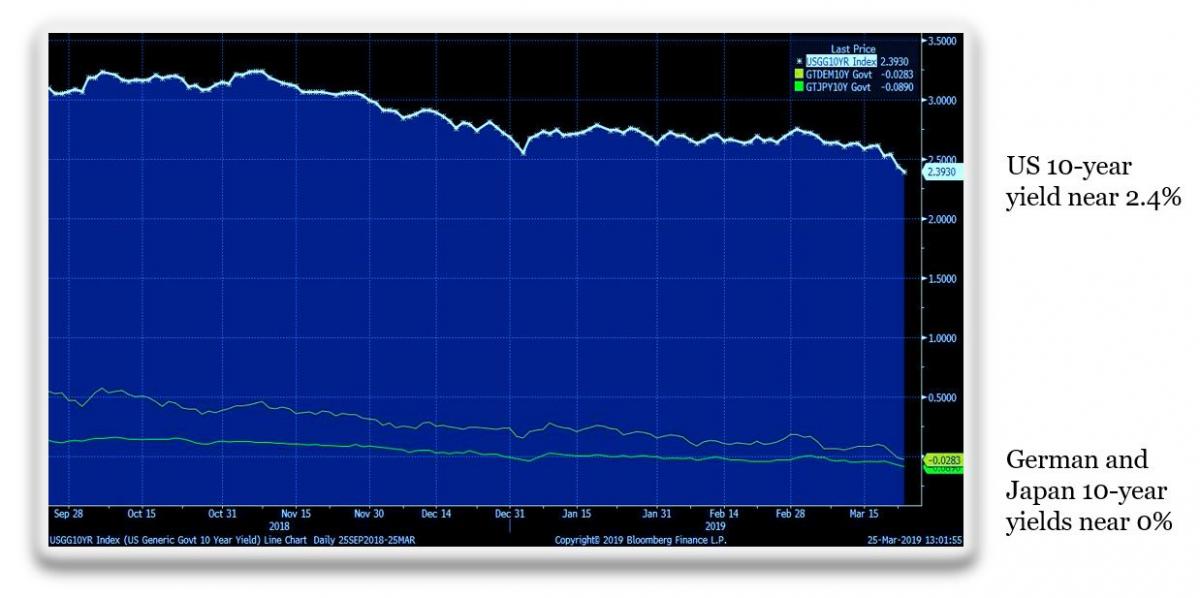

The recent interest rate plunge below 2.5% for the US 10-year Treasury and the inversion of certain short-term and longer-term curves keeps global growth concerns front of mind for investors. The yield environment is certainly challenging, and with yields in other developed countries like Japan and Germany hovering near zero (or even negative) it’s hard to foresee the US yield curve steepening to any great degree. But with global quantitative easing occurring in unprecedented fashion, does an inverted yield curve signal a recession this time around? Maybe, maybe not – but bad news abroad has never led the US into a recession and not every inversion is a harbinger of recession. It is reasonable to think that US stocks may still be the preferred investment vehicle given a healthy consumer and such sparse returns available in the global bond market. Some stabilizing of US yields would be helpful to prevent further curve inversions and ease any recession fears.